FERNANDO DE FRUTOS, CFA, PhD | 21 FEBRUARY 2025

• Every time the market breaks records, investor psychology takes on a special role: euphoria over the profits achieved gives way to fear of a sudden correction.

• The risk premium is a static metric that assumes constant earnings, but high valuations can be justified by robust growth expectations.

• The valuations resemble the uncertainty principle of quantum mechanics, according to which two complementary variables cannot be known precisely simultaneously.

• Determining whether the premium paid is excessive or insufficient in relation to expectations is impossible ex ante, since we only observe the aggregate

After twenty-five years of wandering through the desert, last week the EURO STOXX 50 joined the club of major stock market indices that have reached a new high. This is common for the S&P 500, but it took the Nikkei 225 a whopping thirty-four years to do so.

Every time the market breaks records, the psychology of the investor takes on a special role. The euphoria over the profits achieved gives way to fear of a sudden correction that would erase a good part of what had been accumulated.

Investing at highs generates uncertainty. Without previous references, the terrain is perceived as unknown and, therefore, more risky. It is difficult for us to put new capital to work, but it also hurts us to be left out of the party. The reptilian brain theory partly explains this aversion: evolution has favored incremental progress and a greater sensitivity to losses than to missed opportunities. Hence, the temptation to take profits intensifies as profits grow.

Fortunately, we have the neocortex, which allows us to reason and plan for the long term. Evaluating whether it is prudent to invest at the top requires looking beyond geopolitics, business cycles, and monetary policy. Over the long term, stocks rise if earnings per share do, and corporate earnings are currently at record levels as well.

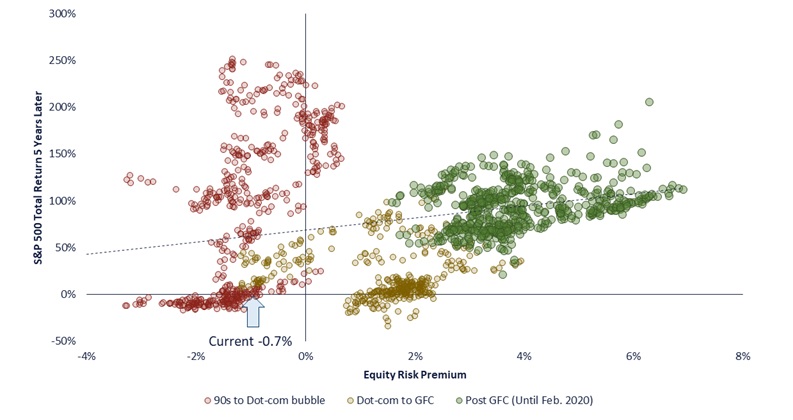

However, prices have grown faster than earnings, which has pushed up valuations. While the P/E ratio suggests the market is expensive, what is really relevant is the comparison with other investment alternatives. The equity risk premium — the difference between the earnings yield and the Treasury bond yield — has fallen to levels not seen since the dot-com bubble.

Back then, the risk premium was as low as -3%. Today, it is close to -1%, after averaging more than 3% over the past two decades. This might suggest caution in equity exposure. However, valuations are only part of the equation. Unlike bonds, equity returns can grow over time. The risk premium is a static metric that assumes constant earnings, but high valuations can be justified by robust growth expectations.

The following chart illustrates this idea: on the horizontal axis, the S&P 500 risk premium at a given point in time; on the vertical, the index’s return five years later. The dispersion of the data suggests that there is no clear correlation between the risk premium and future returns, which reinforces the hypothesis that markets are efficient and reflect the information available at any given time.

In this sense, valuations resemble the uncertainty principle of quantum mechanics, according to which two complementary variables cannot be known precisely simultaneously. Investors pay higher premiums when growth prospects are high and vice versa. Determining whether the premium paid is excessive or insufficient relative to expectations is impossible ex-ante, as we only look at the aggregate.

Historically, a high risk premium (cheap stock market) has been, at best, a sufficient but not necessary condition for obtaining good returns. On the other hand, when the market has been expensive, the results have been very mixed, with both mediocre and extraordinary returns.

At this point, is the market correctly valued? With a US economy that continues to move away from the risk of recession thanks to pro-growth policies and with AI leading a new digital revolution, current valuations could be justified. Only time will tell if reality will exceed expectations or if we have fallen into excessive optimism.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.