Tariffs, power, and membership: navigating the new trade doctrine

BY FERNANDO DE FRUTOS, CFA, PhD | 7 APRIL 2025

• The Global Trade Backdrop: For decades, globalization boosted growth but created deep imbalances—both between countries and within them. With China rising as a strategic rival and trade liberalization stalled since the early 2000s, the United States is now leveraging its unique position to reset the terms of trade.

• Tariffs as Strategy, Not Ideology: While often criticized as consumer taxes, tariffs can be a rational tool for the U.S.—whose domestic market remains its greatest asset. However, the top-down, blunt rollout has created significant uncertainty, disrupting supply chains and leaving investors and businesses in limbo.

• Portfolio Positioning: This is not a time for panic, but for strategic clarity. Diversification is key, and the recent correction has created more attractive entry points. While earnings growth may be impacted in the near term, especially for companies exposed to global supply chains, broad market exposure remains the most resilient strategy.

April 2: A Turning Point in Global Trade

April 2nd may come to be remembered as a watershed moment in economic history. While media coverage has been swift and overwhelmingly critical—understandably, as no country stands to benefit immediately from the policy shift except, perhaps, the U.S.—investors should be cautious not to fall into groupthink.

This piece offers an alternative, non-partisan perspective on what is happening, focusing on the why, the how, and what might come next. It does not seek to pass moral judgment, but rather to help navigate the unfolding landscape. Supporting economic freedom does not mean trade without barriers—it means each party retains the sovereign right to set the terms under which it trades.

How We Got Here: The Unraveling of Globalization

The second half of the 20th century was marked by the liberalization of trade and capital, driving global integration and economic growth. But the benefits were unevenly distributed—between nations and within them.

Trade frictions are not new. In the era of fixed exchange rates, imbalances were addressed through major currency adjustments—think of the Plaza and Louvre Accords, when the United States devalued the dollar to regain competitiveness and reduce trade deficits. Today, with free-floating currencies, the United States is instead choosing to rewrite the terms of trade directly.

The failed Doha Round in 2001 marked the last major attempt to reform global trade—coincidentally, the same year China joined the WTO. Since then, China has absorbed vast manufacturing capacity, strengthening both its economy and military at the expense of industrial jobs in the West. Importantly, China has become the United States‘ primary geopolitical rival. Offshoring benefited global consumers but hollowed out domestic production. In President Trump’s view, the United States no longer benefits from the existing trade terms—and is now uniquely positioned to reset them.

A Country Club Model of International Trade

The United States remains the most attractive internal market globally and runs persistent current account deficits with many trading partners. This makes it the only country with enough leverage to unilaterally demand new terms.

President Trump, who owns and resides in private clubs, appears to apply the same logic to trade: access comes at a price. In clubs, one pays an initiation fee. In trade, one pays a tariff. Clubs also form reciprocal agreements—mirrored in bilateral trade deals.

The administration is leveraging America’s economic might, much like it has wielded the dollar as a geopolitical tool. In global markets, this is not about “fair” competition—it is about power. And power is not evenly distributed.

Debunking Simplistic Economics: A Tariff is Not a Tax

The argument that tariffs are simply “taxes on consumers” misses the nuance. Tariffs are levied on imports, not directly on households. The degree to which prices rise depends on many factors: availability of substitutes, the capacity to reshore production, and the elasticity of demand.

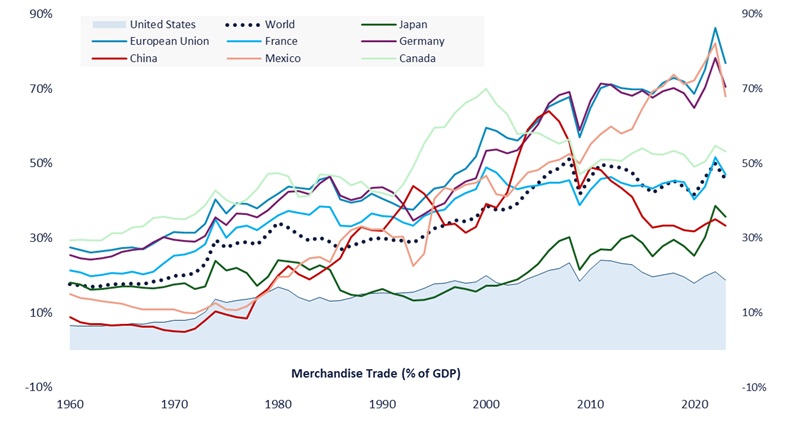

If tariffs stabilize around 10 percent baseline, importers may absorb the cost to protect market share. If they rise significantly higher, some inflation is likely—but even then, it is not an automatic pass-through. Services—which comprise 70 percent of United States GDP—are unaffected, and total trade accounts for just 18 percent of the economy.

Growth may slow, but a recession is not a foregone conclusion. Less importing implies more local production. Meanwhile, tariff revenues could fund tax cuts or help reduce debt servicing costs, softening the macroeconomic impact.

For U.S. trading partners, the impact is more direct: fewer exports, slower growth, and downward pressure on prices. This asymmetry explains both the urgency to negotiate and the risks of retaliating from a weaker position—no surprise, then, that only China, with its state-directed economy, has dared to push back.

Markets and Central Banks Don´t Like Uncertainty

The rollout of the tariffs was rapid and blunt, lacking differentiation between inputs and finished goods. This top-down, “back-of-the-envelope” approach introduces chaos—and invites intense lobbying. Industries will scramble, business models will be tested, and real-time impact data will soon flood into the White House.

Because reciprocal tariffs were also calculated arbitrarily, the administration retains wide discretion to reduce them in exchange for political wins. Markets dislike this level of uncertainty, and valuations will likely remain under pressure until greater clarity emerges.

Even if the shock is not existential for the United States economy, the short- and medium-term effects could be painful. If negotiations stall and supply chains start adapting to the maximalist tariff levels, the long-term costs will rise—and become harder to reverse.

Central banks will remain vigilant, monitoring both inflation and signs of economic weakness. Having misjudged “transitory” inflation in 2022, they will require more evidence before taking decisive action. The so-called “Fed Put” still exists—but it is priced further out of the money.

Currencies: A New Front in Trade Wars?

Currency dynamics may soon shift. Classic economic theory links exchange rates to trade balances, interest rates, and growth differentials. If the new tariffs lead to smaller U.S. trade deficits while growth holds up, there will be little reason to expect meaningful long-term depreciation of the dollar. Tariffs may push U.S. inflation higher while exerting disinflationary pressure abroad, helping to maintain a positive interest rate differential in favor of the U.S.

Ironically, the new trade regime could be partially offset by a realignment in currencies. Expect increasing pressure from the White House on the Fed to lower interest rates—and talk of “currency manipulation” to reemerge.

Don´t Panic—Position Strategically and Diversify Well

The scale of the tariff announcement caught many off guard. It originated from the administration’s most hardline advisers—Trade Advisor Peter Navarro and Commerce Secretary Howard Lutnick—sidestepping more moderate voices like Treasury Secretary Scott Bessent. But if the pain spreads from markets to the real economy, the pendulum is likely to swing back toward pragmatism. The administration is unlikely to continue administering a cure that risks killing the patient.

Trade may be in retreat, but capital flows are more globalized than ever. As individuals, we may feel the economic pinch of tariffs. But as investors, compounding that impact by fleeing risk assets and realizing losses is inadvisable. Regardless of how investors outside the United States feel about President Trump, U.S. equities remain an indispensable part of any global portfolio.

The recent correction has meaningfully reset valuations—especially when considering earnings trends leading into the selloff and the concurrent drop in interest rates. (The equity risk premium has risen by almost 2 percent.) When global earnings resume their upward trajectory—whether soon or further down the line—markets will eventually follow.

In the meantime, there will be casualties. Some business models face existential threats. This is why maintaining strong diversification is critical. This is a time for index investing, not stock picking—tempting as the latter may be.

This is also a moment for clarity, not panic. Avoid herd behavior. Maintain a long-term view—and if you have cash on the sidelines, consider deploying it selectively in this dislocation.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.